Your read progress

How annual £750 savings can grow to over £22,000 for your child by age 18

4 minute read

Updated 22nd October 2025 | Published 28th June 2024

In a new study in collaboration with our sister site, Be Clever With Your Cash, we asked UK parents about their thoughts and approach to saving for their children's future.

In a new study in collaboration with our sister site, Be Clever With Your Cash [1], we asked UK parents about their thoughts and approach to saving for their child’s future.

Parents told us they typically put away £750 each year for their child which could grow to over £22,000 by the time they’re 18 if they pick the top savings accounts.

In this article, we share some other key findings and our tips for getting the most out of providers when it comes to maximising your child’s savings.

Why saving for your child’s future is important

Buying a car, paying for car insurance and the cost of going to university are just some of the financial challenges young people are likely to still be facing in the future.

Parents want to do as much as they can to help their kids get a great start in adult life. That’s why most parents told us that they’re prioritising saving for their child over building their own rainy-day funds.

We found that on average parents have put away £8,002 for their children, compared to their own savings pot of £6,251[2]. Dads are saving double for their kids, compared to mums. But this is generally because women still earn less than men and most leave full-time employment after having children.[3]

Although savings rates have increased recently, it’s likely they’ll drop again later in the year. Choosing the right account now to start building up your child’s savings could make a big difference to the future growth.

The long-term benefits of saving consistently

Saving any amount at any time is always beneficial. But saving consistently helps you make the most of your child’s savings because of compound interest.

Compound interest accelerates savings growth because it creates a snowball effect. Interest is earned on the amount saved and then added to the savings balance. Interest is then calculated on the entire sum, including the accumulated interest. So, as the balance grows with each deposit, even more compound interest is earned pushing the balance up higher.

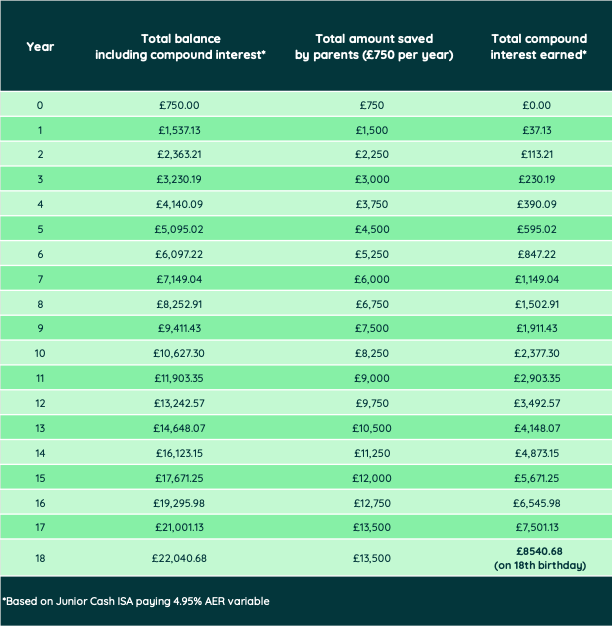

How annual £750 savings can grow to over £22,000

Our colleagues at Be Clever With Your Cash shared that the best Junior Cash ISA is currently with Coventry Building Society, paying 4.95% AER variable (correct as of June 2024)[4].

Let’s look at how £750 saved in this account every year could grow over 18 years.

How to choose the best savings account for your child

65% of parents told us they’ve set up savings accounts for their children. But only one in five (20%) parents are planning to look for a new children’s savings provider this new tax year as a quarter (25%) admit to being confused by which account to choose.

On top of that, nearly a third of parents (28%) said they find the process of moving financial products stressful. But as our example calculation shows, the account you choose can have a big impact on your child’s savings growth, so it’s important to shop around.

To help you find the best rates, our colleagues at Be Clever With Your Cash have recommended their top picks for children’s savings accounts.

Getting a good rate will help you maximise your child’s savings, but there are other factors to consider too. Reading customer reviews on Smart Money People is a great way to see what existing customers think of children’s accounts.

Why parents choose Smart Money People reviews

At Smart Money People, we’re the UK’s most comprehensive customer review site for financial products and services. Our reviews help people just like you to feel informed so you can make smarter financial decisions.

Our reviews complement your wider research on products and providers. They cover a range of areas including price and customer service so you can research what’s most important to you.

You can read or leave financial product reviews with us at any time, simply head to our website to get started.

1. Smart Money People commissioned a survey of 2,000 UK adults who have a savings account. The OnePoll survey ran 12 - 16 April 2024. OnePoll is an MRS Company Partner.

2. According to latest ONS figures UK families have 2 children on average

3. According to recruitment organisation, Hays

4. Rate correct as of 17th June 2024 but is subject to change at any time throughout the life of the ISA which means the actual interest earned could vary. The calculation is based on a rate of 4.95% per annum with £750 being deposited into Junior Cash ISA every year for 17 years. The final amount shown is the estimated balance when the child reaches 18 years old.

Written by Errolyn

Senior Content and Social Media Executive

As Featured By

Join our mission

We use the power of consumer reviews to help increase trust and transparency in financial services and to deliver industry leading insight and events.

Write a reviewRelated financial insights articles

View financial insights.jpg)

State Pension vs Workplace Pension: What’s the difference?

21st July 2026 by Errolyn

Couples that save together stay together

17th September 2025 by Errolyn.png)