Your read progress

Do BDMs still play a valuable role in today's mortgage industry?

3 minute read

Updated 17th September 2025 | Published 22nd January 2024

At the end of November, we released our latest Mortgage Lender Benchmark, covering broker opinions on UK mortgage lenders for the second half of 2023. Our eleventh edition analysed the state of the mortgage industry according to brokers’ views, and included in-depth data and insight from over 790 mortgage brokers.

As a whole, the latest results remained fairly stable. There was only a slight dip from the record broker satisfaction levels seen in H1 2023, suggesting that lenders appeared to have largely coped with the ongoing market turbulence caused by further rate rises in the latter part of 2023.

Alongside our usual benchmarking set of questions, we asked brokers: ‘Do BDMs still play a valuable role in supporting the relationship between brokers and lenders?’. The results overwhelmingly supported the role of the BDM. Here are some of the highlights:

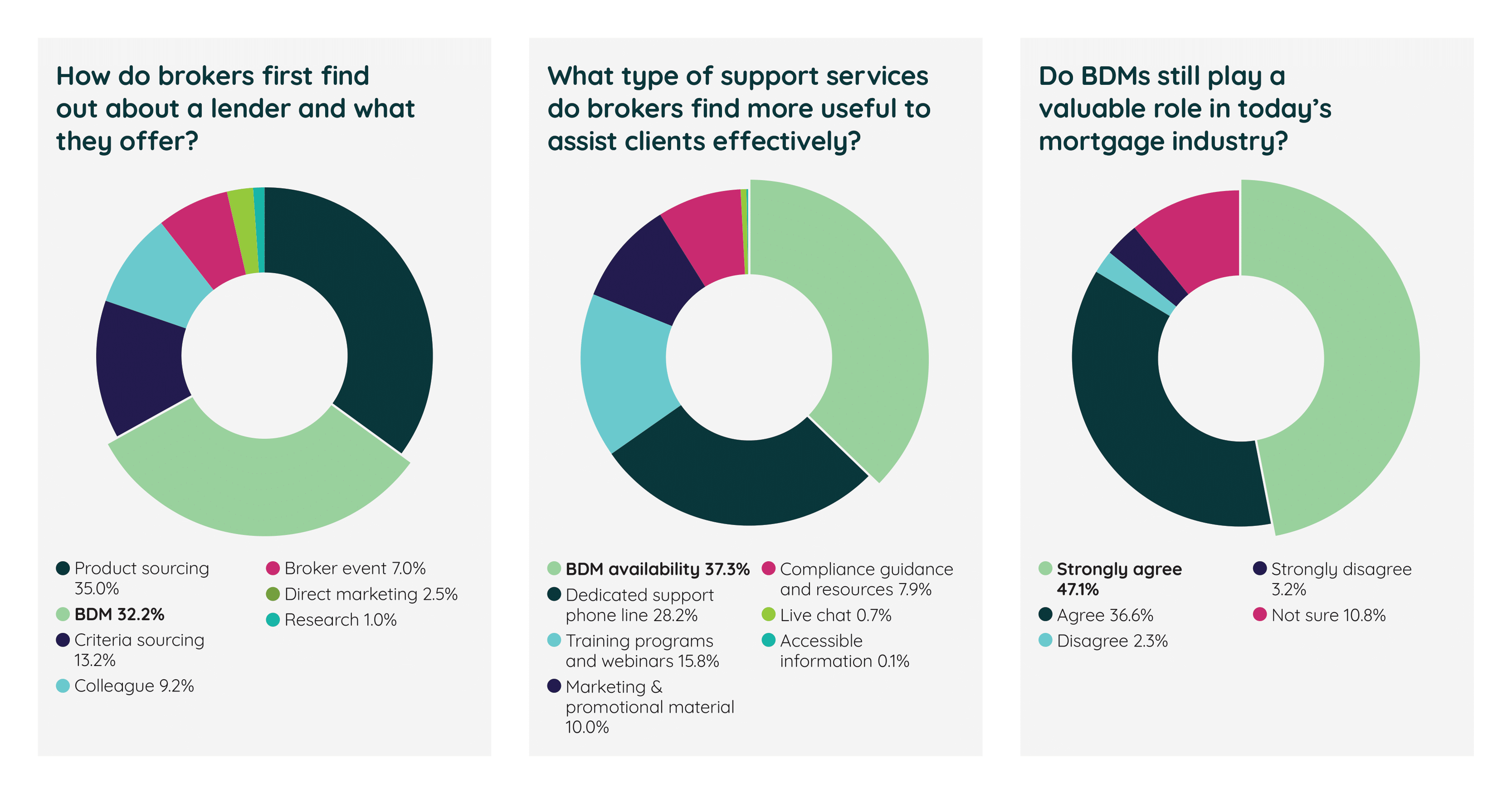

- 83.7% either agreed or strongly agreed that BDMs play a vital role in the industry today.

- Only 5.5% disagreed or strongly disagreed, with the rest unsure.

- 32.2% said they typically first hear about a lender and what they offer from BDMs, with only product sourcing scoring higher (35%).

- 37.3% said BDMs, when we asked brokers what they’d consider as their most valuable form of support service to serve clients effectively, beating the likes of dedicated phone lines, training programs / webinars and live chat.

Despite these encouraging results, it’s clear that some lenders don’t measure up. Whilst the slight majority of brokers (43.3%) were happy, over a third (36.4%) said they didn’t feel their lender gave enough BDM support, with the rest unsure. One major high street bank came in for notable criticism by having no BDM presence at all! In addition, while some comments called out BDMs for not answering the phone or calling back, many brokers sympathised with overworked BDMs covering areas that are too large.

However, even lenders offering BDMs weren’t always necessarily well received by brokers, as many said that BDMs were simply not doing the right things. For example, some brokers said that certain BDMs offer little value with cases and simply quote website criteria.

Others also wanted to be able to speak to the same person to build a relationship, with some sharing examples where inconsistent information had been given by different people. And a number of brokers from smaller firms felt they were being overlooked due to writing less business.

The final area coming in for a lot of attention was the move from in-person BDMs to telephone-based BDMs, meaning less availability on the road. While some brokers seemed comfortable with this change, many blamed the apparent problems with availability and accessibility on the lack of in-person support. Many stated that the level of service they receive on the phone isn’t as good as what they’d get in person. So although it’s clear that brokers understand the need for lenders to evolve, moving too quickly to a hybrid approach may be damaging to lenders’ relationships with brokers.

In summary, brokers clearly still value BDMs. But many feel that some lenders still have work to do. There’s clearly a huge opportunity for lenders to stand out by providing BDMs with good case knowledge who are readily available and accessible.

Written by Darryl

B2B Marketing Manager

Darryl joined us in 2023. He is passionate about ensuring others make good choices with their money using all the information and data available.

As Featured By

Join our mission

We use the power of consumer reviews to help increase trust and transparency in financial services and to deliver industry leading insight and events.

Write a reviewRelated industry news articles

View industry news

Mortgage Lender Benchmark H1 2024: The results

17th September 2025 by Darryl

Looking back at the Building Societies Annual Conference 2024

17th September 2025 by Darryl

Is the industry ready for the final Consumer Duty deadline?

17th September 2025 by Darryl